Are You Planning to Sell Restricted Stock Units This Year? Here's a Few Tax Considerations

Restricted Stock Units (RSUs) are an increasingly common form of compensation for employees, particularly in high-growth industries like technology, healthcare, and finance. Unlike a cash bonus, RSUs offer the potential of stock market upside —often used to align employee incentives with company performance and retention goals.

But for many RSU holders, the taxation of these awards can be deceptively complex, and even a well-timed sale can turn into a tax trap if not reported carefully. When selling RSUs, it is crucial to keep solid records and share them with your tax professional to prevent being taxed on the same income twice.

To subscribe to the MalcolmOnMoney newsletter and receive more content like this, click here.

When RSUs vest, they become taxable as ordinary income based on the fair market value of the stock on the vesting date. This amount is reported on Form W-2 and is subject to income tax withholding, Medicare, and Social Security taxes. If you sell all vested shares immediately, you generally won’t owe additional tax because your sale price is effectively equal to your “cost basis.” But if the stock appreciates or depreciates after vesting, selling the shares generates a capital gain or loss.

If you hold the shares for more than one year before selling, any gain would be taxed at the more favorable long term capital gains rates—which today are 0, 15, or 20%, depending on your gross income. And if held for less than one full year, the gain is considered short-term and will be taxed at your ordinary income rates.

As a result, when receiving and selling RSUs (in particular), it is possible to have income that is both ordinary and a capital gain. Thus, for RSU holders who want to sell, the timing of the sale is only one part of the equation. Most of the risks lie with how the sale is reported on your tax return.

In tax jargon, RSUs are considered “non-covered securities.” This means that neither your stock plan administrator nor your broker is required to report your cost basis to the IRS. So, in many cases, at the end of each year where a sale has occurred, your brokerage will send you a Form 1099-B where the “Cost or Other Basis” field (Box 1e) is either blank or shows $0.

Therein lies the problem. If you or your tax preparer simply copies the numbers from the 1099-B onto your tax return without adjusting your original basis, you will end up reporting a capital gain equal to the full sale proceeds. That means you will essentially pay taxes twice on the same income.

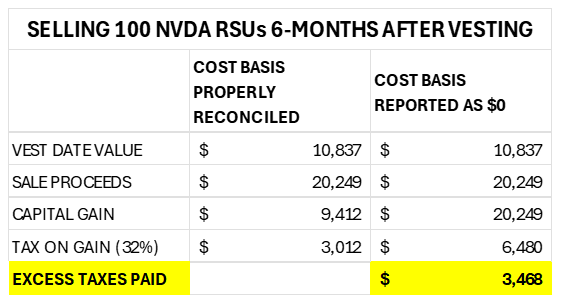

For example, suppose Alex (an NVDA employee who is in the 32% federal tax bracket) has 100 RSUs vest on March 31, 2025 ($108.37/share) and decided to sell them all on October 31 ($202.49/share) of the same year.

If reported properly, Alex would owe approximately $3,012 in short-term capital gains. But if she mistakenly reported her basis as $0 using the data reflected on her 1099-B, she would end up paying more than twice that amount in taxes unnecessarily.

Chart illustrating how incorrect cost basis reporting for RSUs can trigger unnecessary taxes.

To avoid being double taxed, IRS rules require you to use Form 8949 to properly report the sale of RSUs. This form allows you to reconcile the incorrect or missing basis information shown on Form 1099-B with the corrected cost basis.

When filling out Form 8949, sale proceeds are entered as shown on your 1099-B, then the proper basis is inserted. If the Form 1099-B basis is missing or incorrect, Column (g) is where the adjustment must be recorded. This informs the IRS that part of the sale proceeds have already been taxed through your W-2.

Once you have reconciled the numbers, the net gain or loss flows to Schedule D, which tallies up your capital gains for the year. This is the form the IRS uses to determine your total taxable gains and whether you owe additional tax or qualify for a deduction. It also distinguishes between short- and long-term gains, which can affect your final tax liability depending on how long the RSUs are held after vesting.

It is critical that you keep detailed records of each vesting—if you decide to sell any of your shares—as this information can have a tremendous impact on your overall tax bill. Your broker may not track this for you across multiple years, and without accurate documentation it becomes much harder to properly report your cost basis later on.

As an employee, receiving RSUs can be a lucrative opportunity. But it is essential to understand and manage the associated tax implications. By following proper reporting procedures, coordinating with your tax professional and your stock plan administrator, you can navigate RSU sales effectively and avoid the pitfall of double taxation.

*************************

Malcolm Ethridge is the Managing Partner at Capital Area Planning Group, based in Washington, D.C. His areas of expertise include retirement planning, investment portfolio development, tax planning, insurance, equity compensation and other executive benefits.

To subscribe to the MalcolmOnMoney newsletter and receive more content like this, click here.

Disclosures:

The information provided is for educational and informational purposes only, does not constitute investment advice, and should not be relied upon as such. Be sure to consult with your legal advisors before taking any action that could have tax and legal consequences.

Investments in securities and insurance products are:

NOT FDIC-INSURED | NOT BANK-GUARANTEED | MAY LOSE VALUE